MiCA is live, the deadlines are fixed, and regulators are ready to enforce, with fines reaching €20M or 5% of global revenue for non-compliance. For any crypto product operating in the EU or serving EU clients, “wait and see” becomes a liability. With ESMA’s 2025 MiCA Implementation tightening the rules around custody safeguards, incident reporting, and operational resilience, the bar is clear, and it’s high.

This guide is a MiCA compliance checklist: what to implement, the sequence that prevents rework, who should own each task, and how to validate it so compliance becomes a living, testable part of your platform. This is the playbook that helps teams stay licensed, secure, and ready for audits without stalling the product roadmap.

This checklist means a clear path from strategy to execution, starting with the real requirements MiCA imposes on your business. Let’s break those down next.

MiCA Regulation Decoded: What It Means for Your Crypto Business

MiCA is the EU’s rulebook for crypto-asset services — straightforward on paper, unforgiving in practice. It defines how your platform must operate, how you secure user funds, how you communicate with customers, how you test your systems, and how quickly you report incidents when something breaks.

Who MiCA applies to:

Crypto-Asset Service Providers (CASPs) of every size, token issuers, stablecoin issuers, exchanges, wallet providers, advisers, brokers — essentially any business touching crypto-assets in the EU. Even non-EU companies fall under the MiCA regulation the moment they serve EU clients.

What MiCA governs:

Licensing, governance, operational resilience, custody standards, conflicts of interest, AML alignment, transparency rules, disclosures, incident reporting, and the evidence to prove all of it works.

Why startups can’t ignore it:

Regulators now rely on automated monitoring, and MiCA introduces strict reporting deadlines measured in hours, not days. A missed incident report or an unverified custody process can cost more than a production outage.

MiCA compliance isn’t optional. Any crypto or blockchain business offering services to EU users must meet the MiCA regulation requirements, even if your entire team operates outside the EU. The moment you onboard an EU customer, you’re in scope.

Next, let’s break this down into the practical MiCA compliance checklist you can actually use to build and validate a compliant product.

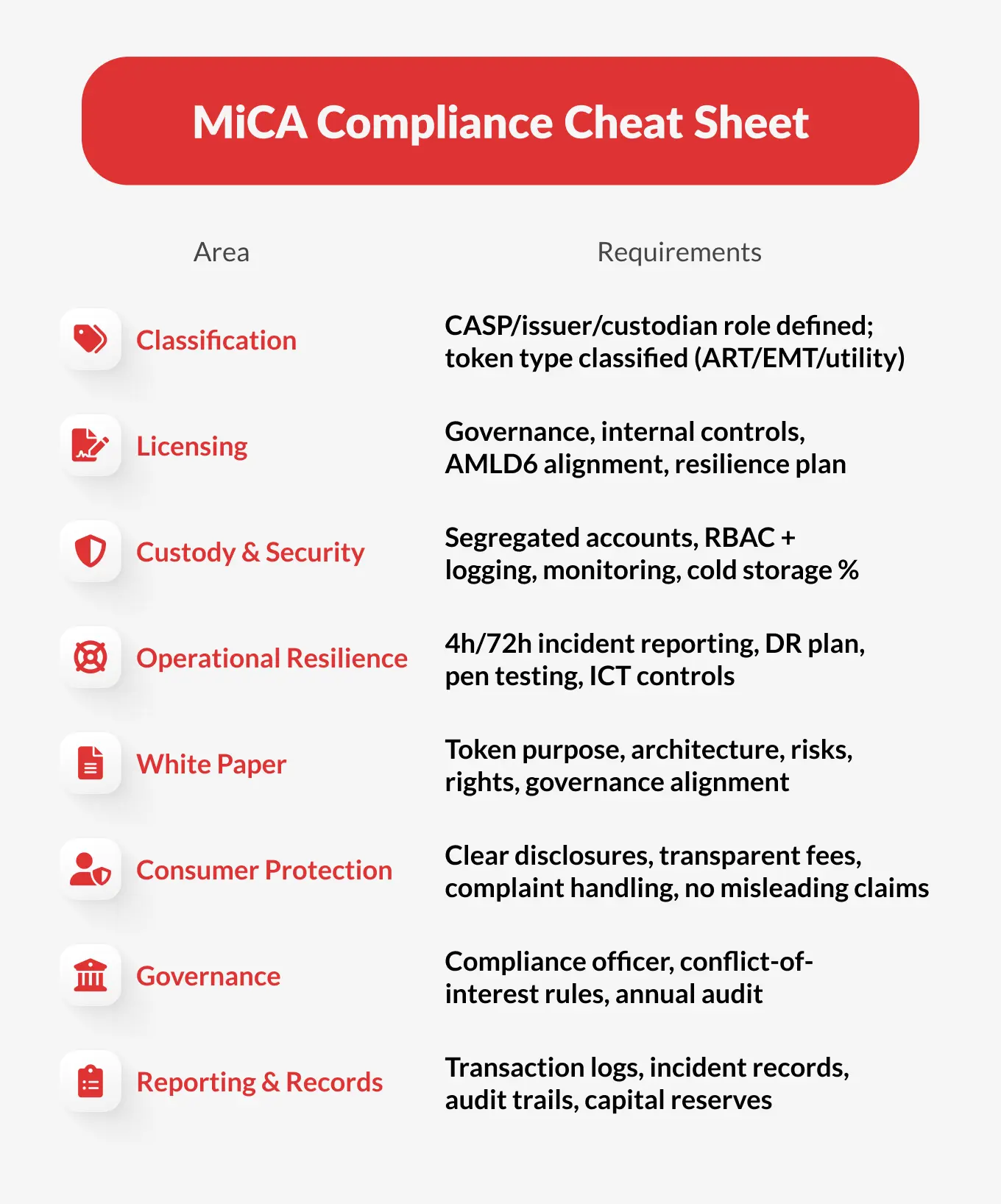

The MiCA Compliance Checklist

Most compliance guides dump requirements in a single list and leave you to figure out sequencing, which is why so many teams misunderstand how MiCA crypto regulation actually works in practice. That approach fails in practice because MiCA implementation has dependencies — you can’t submit a licensing application without classification, and you can’t prove operational resilience without technical controls already in place. This is the part most founders search for — a real MiCA compliance checklist that translates legal text into operational tasks, organized by phase so your team knows what to tackle first.

Phase 1: Classify Your Business and Assets

The fastest way to get lost in MiCA regulation is to misclassify what you are. Classification drives every licensing requirement, every security control, and every disclosure you’ll need later.

Start by identifying whether you operate as a CASP, issuer, adviser, or custodian. Then classify your tokens correctly: utility, asset-referenced token (ART), or e-money token (EMT). The European Commission’s Token Classification Guidance makes this step non-negotiable because mislabeling a stablecoin or an investment-like token can derail licensing before you even submit an application.

Map the regulated activities you perform, such as staking, exchange, custody, execution, and portfolio management. Each one triggers different obligations. And remember a practical detail many teams miss: if your platform lets users hold assets in-app, you’re considered a custodian under MiCA, even if you never touch private keys. The regulation looks at user perception and risk exposure, not your internal architecture.

Phase 2: Build Your Licensing Package

Once classification is locked, assemble the documents regulators want to see before they even open your file. This is your operational blueprint.

You’ll need:

- A governance structure that shows who makes decisions and how responsibility flows.

- An internal control framework that maps risks and mitigation processes.

- An anti-money laundering (AML) program built to meet the 6th anti-money laundering directive (AMLD6) expectations, including screening, monitoring, and escalation flows.

- A business continuity plan that covers outages, data loss, and recovery patterns.

- An information and communication technology controls (ICT) and operational resilience plan aligned with MiCA and Digital Operational Resilience Act (DORA).

- Policies for incident reporting, risk management, and conflicts of interest.

- Financial statements and capital adequacy evidence.

Most startups fail in evidence. Regulators want proof that your controls work. That means logs, monitoring snapshots, test reports, and repeated validation patterns.

Phase 3: Implement Technical & Security Controls

MiCA expects your systems to be secure, observable, and resilient before you apply for a license.

Operational & Security Controls You Must Implement

- Role-based access control with audit-ready activity logging.

- A custody architecture built on segregated accounts and a clear cold-storage percentage.

- 24/7 transaction monitoring that flags outliers in real time.

- Automated fraud rules and AML triggers built directly into your transaction pipeline.

- A penetration testing schedule that satisfies MiCA and DORA’s expectations for recurring security validation, supported by third-party certification when required.

- API rate limits, anomaly detection, and DDOS protection as default safeguards.

- A backup and recovery plan with defined RTO/RPO that engineering can actually meet.

Incident Reporting

Under MiCA, and reinforced by the EU’s 2025 DORA implementation timeline, “major incidents” must be reported fast: an initial notice within four hours and a full report within 72 hours. That requirement forces teams to treat incident workflows the same way they treat deployments — tested, rehearsed, and automated where possible.

Phase 4: White Paper Compliance

If you issue a token, your white paper becomes a regulated disclosure document. It must clearly define the token’s purpose, technical architecture, economic rights, embedded risks, and governance.

Regulators also cross-check it against your marketing and roadmap. If a feature appears in your ads but not in your white paper, or your risk section contradicts your homepage, expect follow-up questions. Build a simple QA review before each release: every marketing claim must match the white paper, every roadmap item must align with the disclosures.

Phase 5: Consumer Protection & Transparency

Consumer protection under MiCA is direct and measurable. If users pay for it, use it, or store it, they must understand the risks.

Practically, this means:

- Clear, accessible risk disclosures.

- Transparent pricing and fees with no fine-print surprises.

- Zero tolerance for misleading claims.

- Monitoring of affiliate and influencer content, just like your own.

- A functional, documented complaint-handling process.

And one rule to live by: if you promote “staking yields”, those yields must be real, reproducible, and verifiable on-chain. Regulators now compare your disclosures with your actual transaction data.

Phase 6: Governance & Internal Controls

Governance under MiCA represents power, responsibility, and documented accountability.

You should implement:

- A compliance officer with true authority and independence.

- A risk officer and a compliance officer for smaller teams, who owns assessments and mitigation steps.

- An annual internal audit cycle.

- Outsourcing controls and vendor risk assessments.

- Staff trading rules that prevent insider misuse through pre-clearance and monitoring.

MiCA is explicit here: if your CTO holds tokens on your exchange lists, that conflict must be assessed, documented, and monitored.

Phase 7: Reporting and Recordkeeping

Ongoing reporting is where MiCA compliance becomes operational muscle. Certain records must be maintained and immediately retrievable.

Track and retain:

- Transaction and execution reports.

- Your complaints ledger.

- Incident logs with detection and remediation history.

- Audit trails tied to access rights and system changes.

- Risk assessments with clear ownership and timestamps.

- Capital reserve data for stablecoin issuers.

MiCA stacks on top of AML laws. Your AML/KYC duties remain governed by AMLD6, which the EU’s 2025 framework update reinforces with stricter monitoring and escalation rules.

The Real MiCA Penalty Traps

MiCA is dangerous because regulators now enforce based on what you can prove, not what you claim to have in place. In Europe’s new crypto regulatory wave, the biggest fines fall on teams that underestimate the evidence and operational discipline MiCA requires from day one.

Below are the real-world traps that trigger enforcement and financial penalties under Article 111 (up to €20M or 5% of global revenue).

1. Evidence Gaps

Most teams assume “having control” is enough. Under MiCA, it’s not. Regulators ask for proof: logs, test outputs, reconciliation records, incident tickets, and monitoring snapshots. When any of this is missing, incomplete, or inconsistent, it’s treated as a compliance failure, even if your processes are technically correct.

This is the number-one pattern highlighted in ESMA’s Market Abuse Monitoring Report, where missing evidence surfaced as the top trigger for supervisory action.

2. Token Misfires

Many startups classify tokens based on product narrative rather than MiCA definitions. That’s where penalties start. Teams get in trouble when a token marketed as a “utility asset” behaves like a payment token or a claim on underlying assets. When regulators detect a mismatch, you face both fines and mandatory reclassification, which can freeze product operations for weeks.

3. Change-Related Breakage

MiCA assumes your platform changes often; it also assumes every change is tested for compliance impact. The trap: a developer updates a feature, adjusts a fee, modifies an API endpoint… and unintentionally breaks a disclosure requirement or operational safeguard.

If you can’t show a traceable review process for these updates, regulators treat it as negligent governance.

4. Mixed Messages

The inconsistency gets companies fined. If your app shows one risk level, your website shows another, and your white paper references an outdated model, regulators see it as consumer deception. They now rely on automated scanning tools to detect inconsistent claims across channels.

5. Bad Records

MiCA demands multi-year retention of operational, transactional, and governance records. Startups are fined for storing incomplete, unsearchable, or poorly structured data that can’t be produced during inspection.

“What did your fraud engine flag in May 2024?”

If you need more than 10 minutes to answer, you look non-compliant.

6. Missed Escalations

Teams often ignore small anomalies because they’re “handled internally”. MiCA regulators look at patterns over time:

- A minor outage

- A checksum mismatch

- A delayed reconciliation

- A suspicious cluster of transactions

Individually, it’s harmless, but if it’s repeatedly ignored,regulators treat it as systemic operational weakness, and that’s when penalties escalate.

7. Undisclosed Conflicts

Compliance relies on people. Executives trading assets listed on your platform, advisors receiving token allocations, and a founder with a side project that overlaps with exchange operations are all manageable under MiCA, if documented. Teams get fined when they fail to show monitoring, disclosure, and periodic review.

A Practical MiCA Compliance Plan

MiCA can feel like a heavyweight project, but most early-stage teams don’t need enterprise-scale compliance from day one. What they need is a layered, efficient, testable setup that satisfies regulators without suffocating product velocity. Here’s how to do it without watching your budget evaporate.

Build Controls in Layers

Founders get into trouble when they try to implement everything at once. MiCA doesn’t require that. A phased approach keeps your roadmap moving while your compliance posture grows steadily.

- Start with licensing essentials: governance, internal controls, and risk documentation.

- Move to custody and security, where most engineering efforts live.

- Automate reporting and monitoring last, once your operational patterns stabilize.

A layered rollout means fewer rewrites, fewer expensive surprises during audits, and a much cleaner path to demonstrating that your platform is MiCA compliant when regulators review it.

Use Modular Tools

Enterprise compliance platforms look impressive but often cost more than an entire development sprint. Startups need modular, replaceable components.

Examples of modular tool types:

- Identity verification modules

- AML monitoring engines

- Logging and SIEM components

- Policy/version-control systems

- Incident-reporting workflows

You get flexibility, lower costs, and less technical debt. And when your platform scales, each module can scale independently.

Outsource Anything That Slows You Down

Some parts of MiCA compliance are essential, just maybe not for your team to do in-house.

You can outsource:

- Internal audits, so you avoid tunnel vision

- Legal review, to keep documentation regulator-ready

- Penetration testing, for unbiased security validation

- AML transaction monitoring, if you don’t want to maintain rule engines yourself

This keeps your developers focused on the product, without drowning in non-stop compliance tasks or losing time firefighting avoidable blockchain security issues.

Validate Everything With QA

This is where teams win or fail. Controls are meaningless if they’ve never been tested. MiCA expects proof, including working logs, passing test runs, and validated flows.

Compliance without testing is wishful thinking. Run validation cycles every release: custody flows, AML triggers, incident reporting pipelines, reconciliation logic, identity checks. Teams that already use blockchain testing services for smart contracts or infrastructure testing can extend the same mindset to compliance workflows. The payoff is huge: fewer incidents, stronger evidence, and far smoother licensing reviews.

We’ve seen this firsthand. When providing QA services for ICONOMI’s crypto asset management platform, we helped optimize their web and mobile onboarding flow, reducing user drop-off by 15%. But beyond usability, we verified the platform’s security and compliance readiness across multiple layers:

- Identity Verification (KYC): We validated document upload functionality across multiple formats, testing “negative scenarios” (poor lighting, incorrect IDs) to ensure error messaging was clear and the retry logic was flawless.

- Geo-Fencing & VPN Detection: To ensure compliance with regional restrictions, we tested the platform’s behavior against VPNs, verifying that access was strictly controlled in accordance with location-based regulations.

- Access Security: We validated that password criteria were not only enforced but clearly communicated, preventing weak credentials from compromising the platform’s first line of defense.

- Edge Case Testing: By intentionally inputting unexpected data (special characters, oversized files), we pushed the registration flow to its limits to uncover and patch hidden vulnerabilities.

Turning MiCA Regulation Into Momentum

MiCA is in place to filter out the careless builders. Teams that treat compliance as part of the product, not a layer of bureaucracy, end up with stronger platforms, cleaner architecture, and far fewer surprises during audits. When you implement the controls and validation cycles outlined above, your product becomes safer by design, regulators trust you faster, and users stop asking, “Is this legit?” You earn the right to scale across the entire EU with a single license, and that’s worth more than any workaround.

If you’re shaping your MiCA setup and want a seasoned pair of eyes on the process, you know where to contact us.

See how we helped a crypto platform boost stability, fix critical issues, and strengthen its readiness for regulatory demands